Love It or Hate It, You Don’t Understand It

By Jack Minchew

Everyone seems to have an opinion on the Patient Protection and Affordable Care Act (ACA) of 2010. Pundits and politicians give speeches and argue endlessly over it, and tempers always seem to rise when someone mentions the ACA. Think you missed out on the biggest political controversy in recent memory? You probably didn’t. Outside the rarified world of inside-the-beltway policy analysis, President Obama’s controversial healthcare overhaul is better known by the slightly derisive and infinitely catchier “Obamacare.”

Passed in 2010 as the result of an unprecedented Democratic majority in Congress and approved without a single Republican vote, Obamacare is certainly a product of its divisive times. Depending on who you ask, the ACA will lead either to the death of the American economy and the explosion of the national debt, or skyrocketing life expectancies and the end of poverty. Dig a bit deeper, however, and you’ll probably realize that other than the cable talking points, very few people have a firm grasp of what exactly Obamacare does and how it affects everyday citizens.

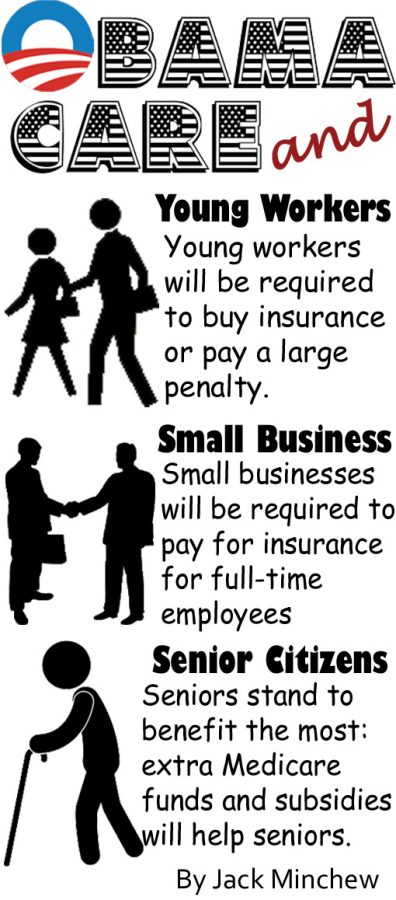

While the ACA is certainly a major change to the US medical system, it is different from a socialist, single-payer universal healthcare program in the European model, where the government pays for all medical expenses for every citizen. Instead, the ACA works by requiring every citizen to either have health insurance or pay a penalty, a controversial provision known as the individual mandate. Insurance coverage can come from an employer, a family member’s employer, or through existing government programs such as Medicare and Medicaid.

Citizens who do not have insurance through any of these options will need to purchase their own insurance on government-approved “healthcare exchanges,” websites that allow individuals and small businesses to compare different insurance plans that all meet mandatory federal standards. Insurance plans are divided on the exchanges into bronze, silver, gold, and platinum levels based on the split between monthly payments (premiums) and out-of-pocket costs (co-pays and deductibles). Bronze plans have the lowest monthly payments, but the highest out-of-pocket costs, while platinum plans have the highest monthly payment and the lowest out-of-pocket costs. Open enrollment on these exchanges begins on October 1st and continues until March 31st.

Those who opt to pay the penalty instead of purchasing insurance will pay a fee of $95 a person per year or 1% of household income, whichever is greater. In Loudoun County, where the median household income is $127,192, this would cost an average person without insurance $1,271.92 a year. By 2016, the penalty jumps to $695 per person or 2.5% of household income. In Loudoun, this would be over $3,100.

Other provisions of the bill prevent insurance companies from denying coverage based on pre-existing conditions and allow children to stay on their parents’ insurance plan until the age of 26. Another controversial provision is the so-called “employer mandate”, which requires all businesses with more than 30 full-time employees to provide insurance to their employees. Some small and medium sized businesses have responded by cutting employees or bumping full time employees to a part-time status.

As most provisions of “Obamacare” come into effect over the next few months, students who enter the workforce after high school or college will encounter a healthcare field far different from that of their parents or even older siblings. While the ACA does provide some benefits for young adults, such as allowing them to stay on their parents insurance until the age of 26, it also can harm young workers, who are frequently uninsured, with the high penalty.